**** Davis follows:

The U.S. lost its lead in batteries 30 years ago when it stopped making consumer electronics devices. Whoever made batteries then gained the exposure and relationships needed to learn to supply batteries for the more demanding laptop PC market, and after that, for the even more demanding automobile market. U.S. companies did not participate in the first phase and consequently were not in the running for all that followed. I doubt they will ever catch up.Subsidized capitalism conceals the real problem, which is the weakening of the overall social environment in which innovation and sustainability take place. It has been weakened by social underinvestment. Grove calls explicitly for jobs policy -- for "jobs-centric" leadership.

Fortunately, physicians no longer believe that bleeding the sick will make them healthy. Unfortunately, many of the makers of economic policy still do. And economic bloodletting isn’t just inflicting vast pain; it’s starting to undermine our long-run growth prospects.Keynesians care about the development of society, and are confused and enraged by the casual blowing off of these concerns by policymakers in the US and the EU alike. "Well, this is a miserable step in the wrong direction" says Jeffrey Sachs, starting a denunciation of both parties in the US. "From a self-preservation angle, this is lunacy," notes David Dayen.

Good job Congress!

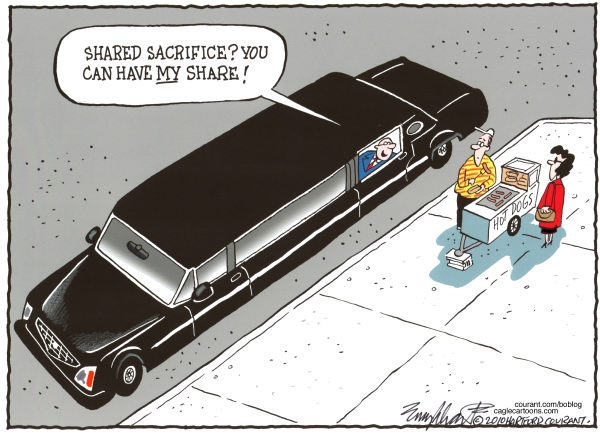

Way to take it from your new Republican Masters! Not since Jack sold his cow for some magic beans has a deal like this been made by our "leadership" where families earning between $35,000 and $64,000 go $7,800 further into debt to get a $613 tax break while families earning between $5M and $10M get $38,590 and families earning $50M to $100M get $380,590 and families (or Corporations, of course) earning $500M to $1Bn get $3,859,000 or about 12,590 times more than the average middle class family but, then again, they deserve it because – they are that much better than you are!

Face it, unless you are in an income category where your tax benefit has 5 digits, you are what George Orwell (who worked in England’s Ministry of Propaganda) called a "Prole." In 1984 the Proles (proletariat) were the vast majority of the populace, the working class of Oceana. Though the proles are the majority, they are unimportant. The Party explicitly teaches that the Proles are "natural inferiors who must be kept in subjection, like animals". As one of the Party Leaders observes: "the relative freedom of working-class people is merely a symptom of the contempt in which they are held". . . .

You’re not going to be any trouble are you? Enjoy your $613, little people. That’s what, about a month’s worth of gasoline and cable TV? Congratulations on your voting acumen – you certainly have gotten the Government that you deserve! . .. .

Congressman Ryan Paul . . . points out: "Whose money is this after all?" It’s not your money that your family is going $7,800 further into debt to protect – it’s THEIR money. THEY earned it and THEY are darned well going to keep it. "Hey," you might say, "I work for THEM – didn’t I make that money and isn’t this OUR country that’s in debt and needs responsible fiscal policy?" Well, that’s just Commie talk and you’d better watch yourself – we’ve already sent your name of to HomeSec so consider yourself on notice…

The Proles in this country are dumb enough but what amazes me is the people who support the tax cuts thinking you are "one of THEM" when "they" look at you the same way you step over a homeless man in the streets. $858Bn is the NATIONAL Debt that we are taking on to fund these cuts. The cuts work out to about 0.75% of your income and your family share of the additional debt burden is $7,800 so, unless you are making AT LEAST $1M PER YEAR as a corporation or individual, this tax cut is a net loss for you. Once you clear that $1M hurdle, it’s all gravy flowing uphill to your plate! Even better if you are a "Corporate Citizen" – you have no real debt obligation to this nation because, like Haliburton and many, many others – you can simply move whenever you want – to avoid taxation AND prosecution!

As Bloomberg proclaims today "It’s a Great Time to Be Rich,"

The central bankers want us to think their fountains of unlimited imaginary money are our sole hope of escaping yawning pits of economic hell. For these apparatchiks, it's all about hanging on to the levers of power any way they can.

The private bankers claim that if we just turn them loose from the stranglehold of post-crash regulation — and allow them to tangle the world in a impenetrable web of insanely profitable derivatives and bonds again — they will plant our feet firmly on the road to financial nirvana.

Here its class war on Wall Street, not just between Wall Street and Main Street.

To these guys, you and I are just foot soldiers and cannon fodder. Our jobs, homes, wealth, and health? Collateral damage.

We as a society must stop pretending. Most of us think that we still have money in the bank to protect, so we go along with the game of extend and pretend. For some of us, the game has already ended. The rapacious zero interest rate policy that I call Bernankecide has already robbed millions of savers of their life savings. This is the reality that has yet to hit home for many Americans who are content to wallow in the status quo. Unfortunately, the longer it takes for them to wake up, the worse their, and our, fate will be.

My mother and millions of other senior citizens are among the victims of the game that policy makers and those who empower them are playing. Their life savings are gone because Bernankecide, the financial genocide of the elderly, forced them to spend their principal. Now the government is indirectly confiscating 8% of my income because I must support my mother. That percentage is likely to grow as her health deteriorates.

Millions of other boomers are in the same boat. They are forced to pay this immoral hidden tax because Ben Bernanke decided that the innocent must pay for the sins of the guilty. While Bernanke’s ZIRP goes on allowing the banksters to continue to collect their fat bonuses, it steals the savings of millions of Americans, eliminates their disposable income, and cuts the spending power of millions of others who must now support those rendered destitute. The guilty benefit, and the innocent are punished.

Bernanke knows that, yet he continues to side with the criminal bankers in support of the financial genocide of the super elderly, and their children, the baby boomers who must increasingly support them.

Decisions are being made that are wrecking US infrastructure. Expert warnings are everywhere. Decisionmakers remain oblivious. People are drawing the obvious conclusions, and are hearing the voice of doom. Charles Simic starts a recent essay by saying, "I can’t remember when I last heard someone genuinely optimistic about the future of this country."

Decisions are being made that are wrecking US infrastructure. Expert warnings are everywhere. Decisionmakers remain oblivious. People are drawing the obvious conclusions, and are hearing the voice of doom. Charles Simic starts a recent essay by saying, "I can’t remember when I last heard someone genuinely optimistic about the future of this country."the financial crisis produced a pattern of rapid economic decline and slow employment recovery quite unlike any post-war recession – it looks much more like a mini-depression of the kind the US economy used to experience in the 19th century. In addition, the fiscal costs of the disaster in our banking system so far amount to roughly a 40 percentage point increase in net federal government debt held by the private sector, i.e., roughly a doubling of outstanding debt.

Adjustments to our regulatory framework, including the Dodd-Frank financial reform legislation, have not fixed the core problems that brought us to bring of complete catastrophe in fall 2008. Powerful people at the heart of our financial system still have the incentive and ability to take on large amounts of reckless risk – through borrowing large amounts relative to their equity. When things go well, a few CEOs and a small number of others get huge upside.

One side of American politics considers the modern welfare state — a private-enterprise economy, but one in which society’s winners are taxed to pay for a social safety net — morally superior to the capitalism red in tooth and claw we had before the New Deal. It’s only right, this side believes, for the affluent to help the less fortunate.Mais non! A major project for progressives is fix Krugman's incorrect alternative to the Right: it's not that the left wants safety nets, it's that the current accounting for value creation is completely distorted, leading to misappropriation of income in the first place. Krugman's formulation guarantees that liberals / leftists will lose, since it grants the genesis claims of the Right and wants to weaken them. It also guarantees the great divide he laments, not because the two sides have incommensurable premises, but because they have the same premise. No conservative has a reason to think of the left as having an alternative philosophy of labor and value that would actually change the position of regular people in society. The alternative just seems like the "bleeding heart:" version of conservatives.

{kind=link}